Working Papers

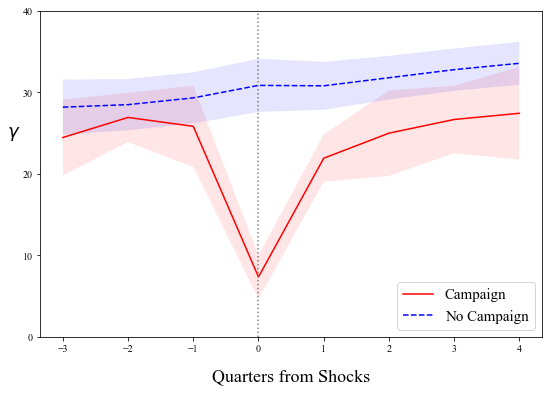

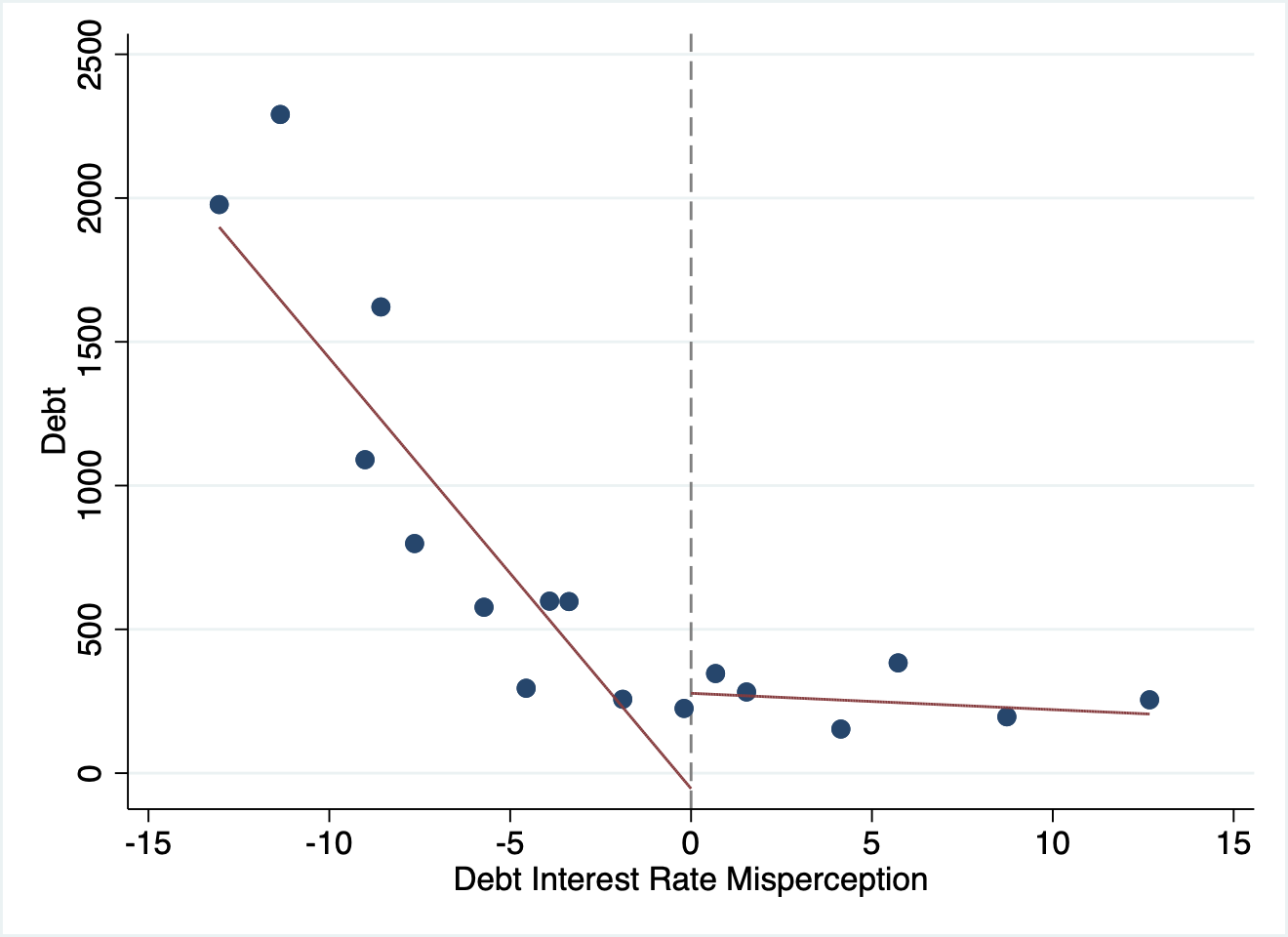

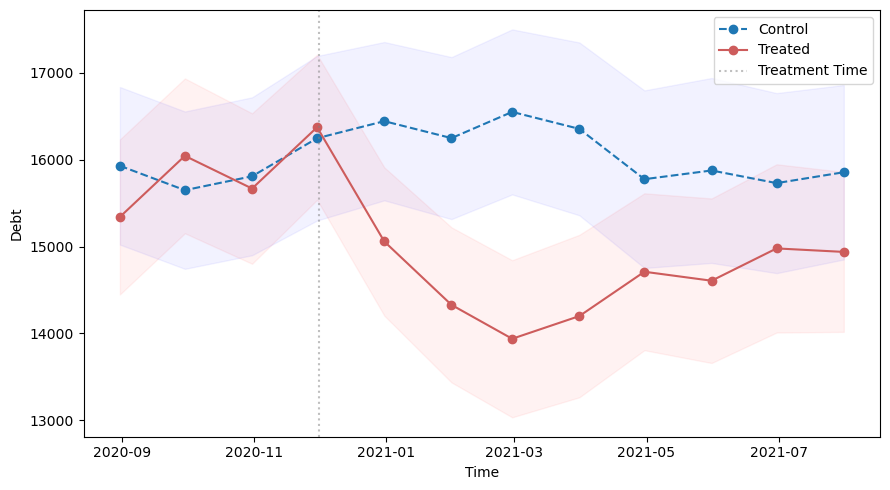

“Cost Misperception: The Impact of Misunderstanding Credit Card Debt Expenses,” single authored, April 2026, Major Revision (2nd round) at Management Science (draft)

Abstract

This paper investigates consumer misperceptions of credit card debt interest costs using administrative data, surveys, and randomized controlled trials. Our findings indicate that borrowers exhibit inaccurate perceptions of the interest costs of unsecured debt, resulting in substantial debt accumulation. A one percentage point lower perceived interest rate leads to 5% higher credit card debt relative to the pre-treatment average. These misperceptions are likely to stem from mistakes driven by financial literacy, particularly in luxury spending decisions, rather than imperfect knowledge of current debt levels or liquidity constraints.

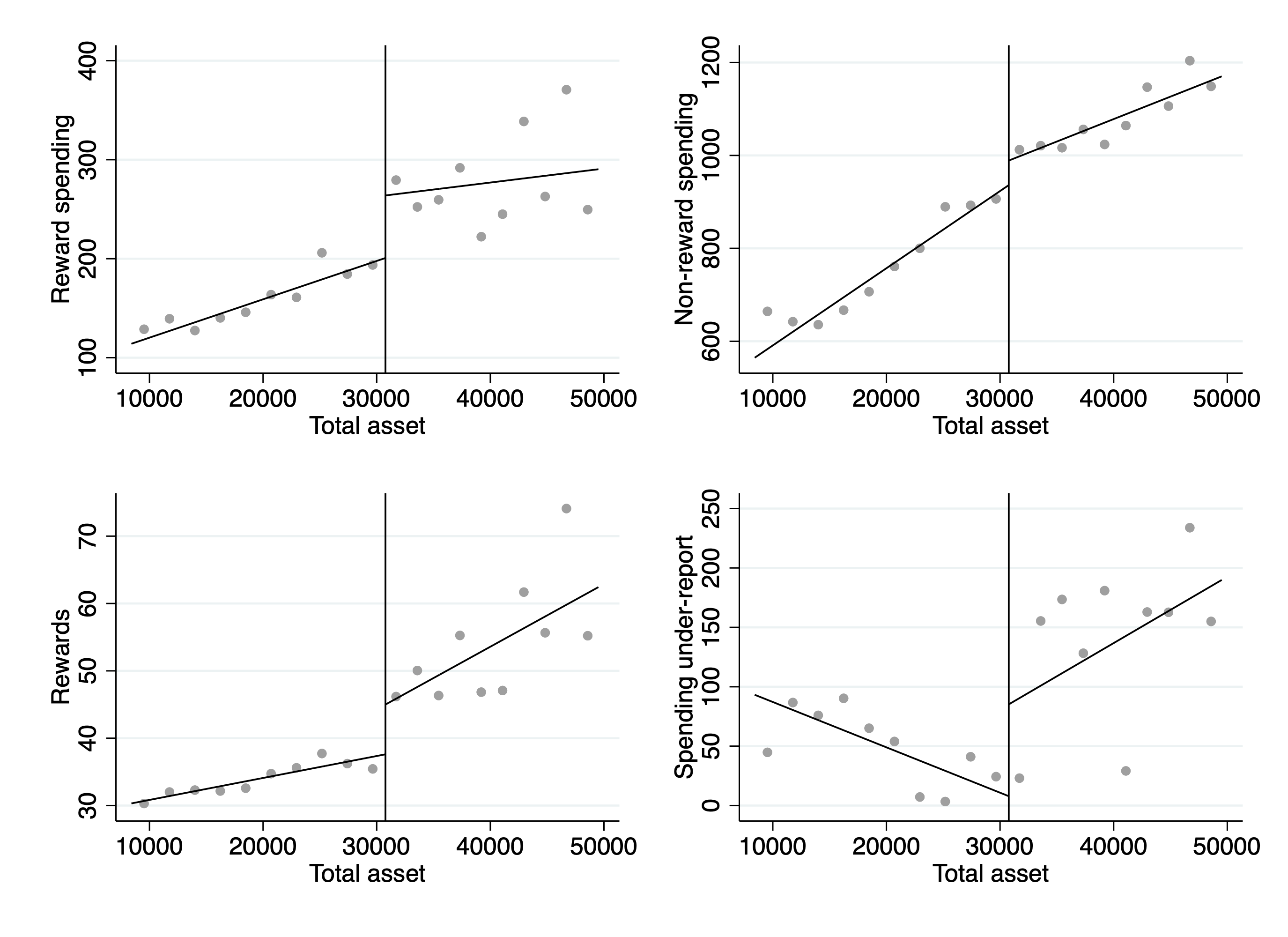

“Rewards and Misperceived Spending: Experimental Evidence from Credit Cards,” single authored, January 2026, Major Revision at Marketing Science (draft)

Abstract

Using proprietary data, a survey, and an experiment with a major bank in China, this paper studies how credit card rewards affect perceived and actual consumer spending. A larger reward variety increases spending in both rewarded and unrewarded categories. While consumers accurately predict rewarded spending, they tend to underestimate total spending. A potential channel is that consumers overlook follow-on purchases that are complementary to the initial rewarded purchases. This misperception distorts consumption and incentivizes firms to offer excessive rewards, generating cross-subsidies from naive to sophisticated consumers.

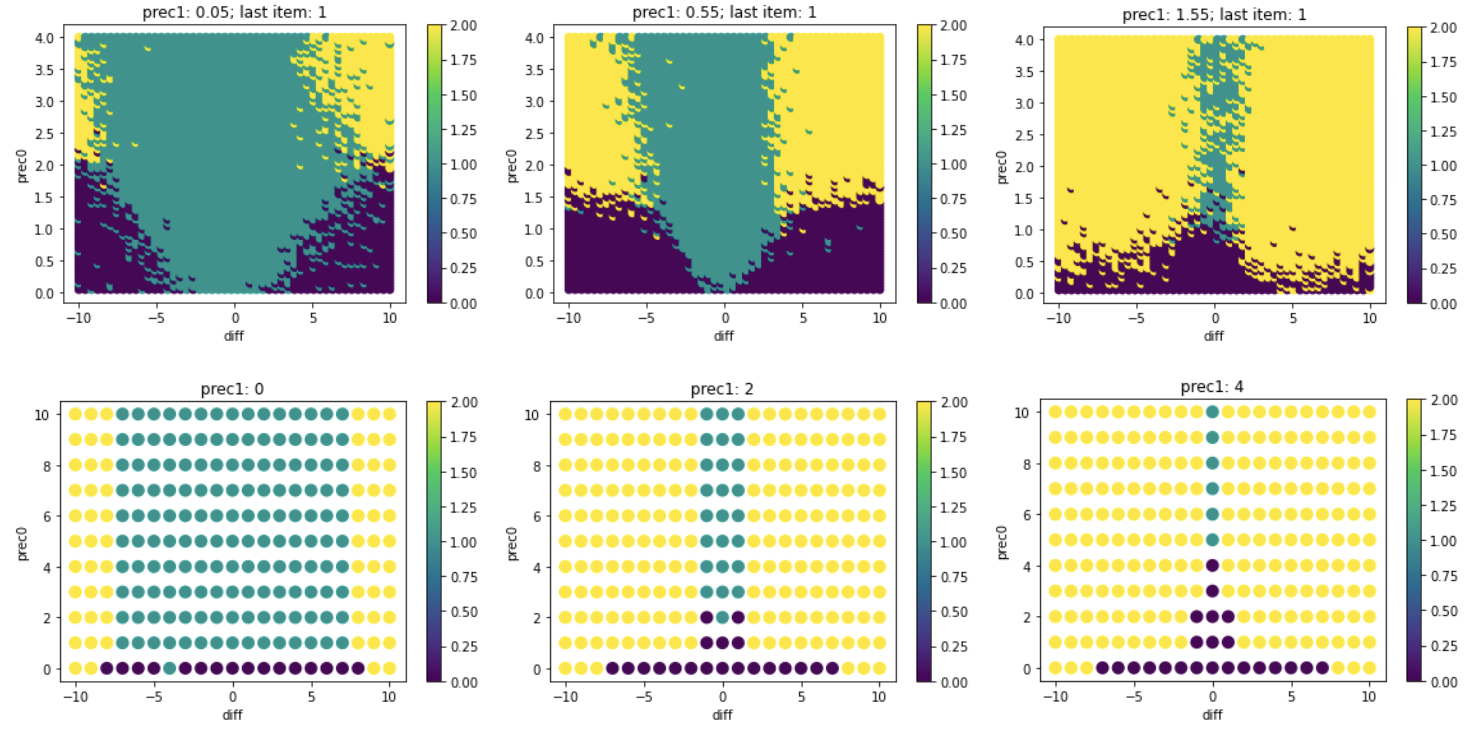

“An Empirical Model of Endogenous Attention,” with T. Tony Ke and J. Miguel Villas-Boas, April 2026 (draft)

Abstract

Before making a choice, individuals can gradually gather information on multiple different possible alternatives. Analysts may observe how long individuals spend gathering information on each alternative, when they switch from one alternative to another, and when they ultimately make their final choice. We develop an empirical model on this choice process, endogenizing the choice of which alternative the individual obtains information from at each point in time, and estimate the model with data from eye-tracking experiments. The empirical analysis yields estimates of the relative size of search costs, attention switching costs, and informativeness of search for information. Counterfactual analysis shows that higher attention switching costs reduce search duration and induce fewer attention switches; in comparison, higher search costs also reduce search duration but induce more attention switches. The model also delivers that there is a positive correlation between attention to an alternative and the likelihood of that alternative being chosen, through the individuals choosing to learn more about the alternatives for which the individuals have beliefs of a higher preference.

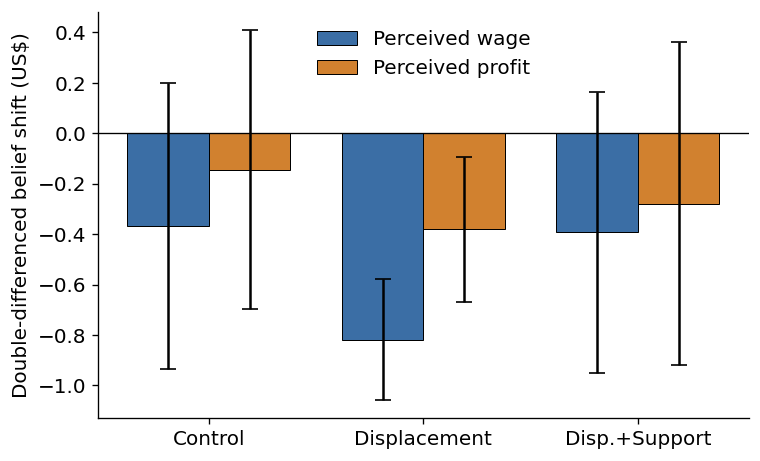

“The Missing Wage: Labor Income and Consumer Aversion for AI-Generated Products,” with Song Lin and Mingduo Zhao, July 2026 (draft available upon request)

Abstract

(Preliminary) When production shifts to generative AI, the product can stay the same while the wage behind it disappears. We show that consumers price this missing wage: beliefs about the labor income a product generates for workers are a component of demand. In an incentive-compatible experiment, 5,015 participants price T-shirts identical except for a human-versus-AI label. The AI label lowers willingness to pay by \$4.18 (23%) and cuts the labor income consumers believe reaches workers by 29%, while barely moving perceived seller profit. A randomized triple-difference identifies the channel causally: human laborer displacement information deepens the penalty by \$1.71, and a promise to redistribute thirty percent of the AI surplus to displaced workers closes three quarters of that increase. The AI-averse preference is distributional: the penalty is concentrated among consumers who place the most weight on workers' welfare, and it responds to restoring the wage in addition to displacement information alone. Made-by-AI disclosure is therefore not demand-neutral, but its cost is partly recoverable: firms and platforms can restore such a penalty by credibly sharing AI's gains with the workers it displaces.

“Information Silos on Social Media: Experimental Evidence from TikTok,” with Wenbo Wang and Zijun (June) Shi, July 2026 (draft available upon request)

Abstract

(Preliminary) Algorithmic recommender systems are widely accused of trapping social media users in self-reinforcing information silos. We introduce an individual-level Information Silo Index that decomposes silo intensity into intrapersonal topic variety and interpersonal divergence from population norms, measured via screen-recorded browsing data from $1{,}268$ TikTok users in a randomized field experiment. We document an awareness gap where users systematically underestimate their silo depth. Disclosing users' own topic coverage causally changes behavior: treated users engage a $2.7$ percentage point larger share of served content, while effects on the silo indices themselves are directionally consistent but modest. Appending persuasive framing to the same disclosure adds no aggregate response, and heterogeneity analyses suggest why: personalized scientific feedback broadens exploration for distinction-seeking consumers but backfires among users whose self-perceptions are already accurate, so subgroup responses cancel within arms. Platform nudges aimed at algorithmic de-siloing should therefore rely less on persuasive content and align richer framing with users' latent social motivations.

Work in Progress

“Income Misreporting in the Credit Card Market,” with Xiao Yin

Abstract

(Preliminary) In the process of acquiring credit cards, consumers often self-report their income levels, a practice that tends to be prone to unverified overstatements. We empirically investigate into the existence of such income misrepresentation and assess whether financial institutions take this potential exaggeration into account. Collaborating with a leading commercial bank in China, we survey consumers on their income growth rates. By utilizing these reported growth rates and current incomes, we infer the consumers' actual income at the time of their credit card application. Our findings indicate a significant degree of income over-reporting among consumers, with an average exaggeration of approximately 30%. Further, we employ a quasi-experimental approach to determine the causal effect of this income misreporting on the allocation of credit limits. Our results suggest that the bank does, in fact, take into account such misreporting behaviors: income exaggerated by 10% decreases credit limit by around 100 US dollars. This study provides insights into consumer behaviors in credit card applications and the corresponding response of financial institutions.