Working Papers

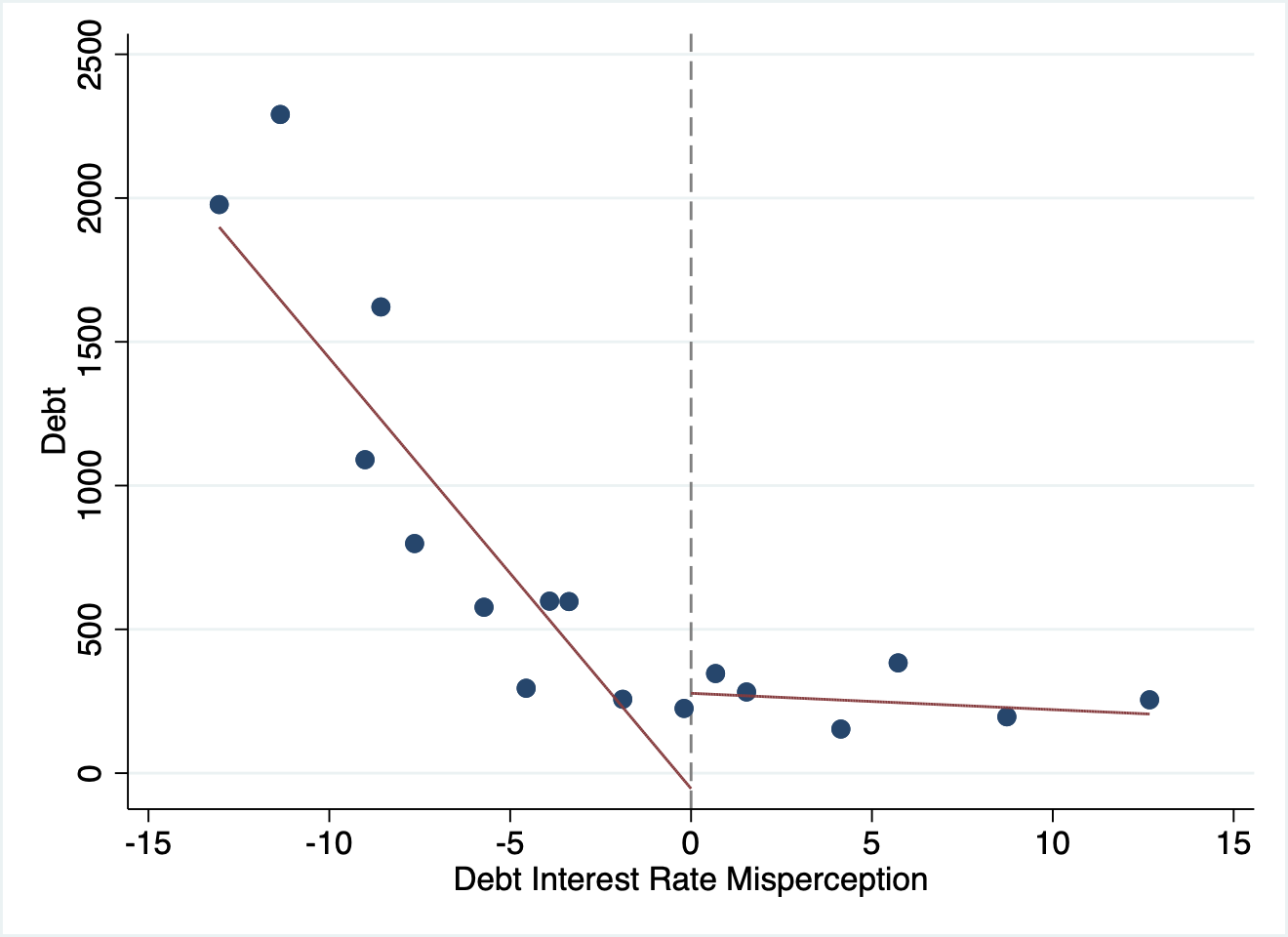

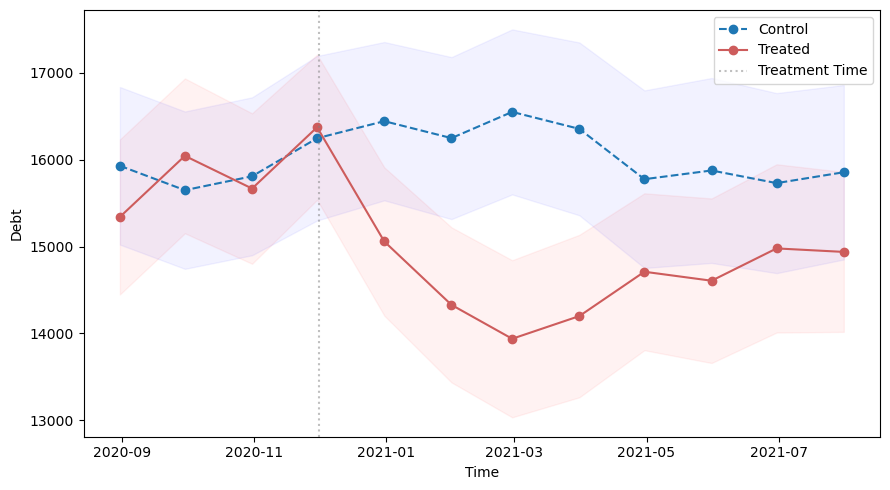

“Cost Misperception: The Impact of Misunderstanding Credit Card Debt Expenses,” April 2026, Major Revision at Management Science (draft)

Abstract

This paper investigates consumer misperceptions of credit card debt interest costs using administrative data, surveys, and randomized controlled trials. Our findings indicate that borrowers exhibit inaccurate perceptions of the interest costs of unsecured debt, resulting in substantial debt accumulation. A one percentage point lower perceived interest rate leads to 5% higher credit card debt relative to the pre-treatment average. These misperceptions are likely to stem from mistakes driven by financial literacy, particularly in luxury spending decisions, rather than imperfect knowledge of current debt levels or liquidity constraints.

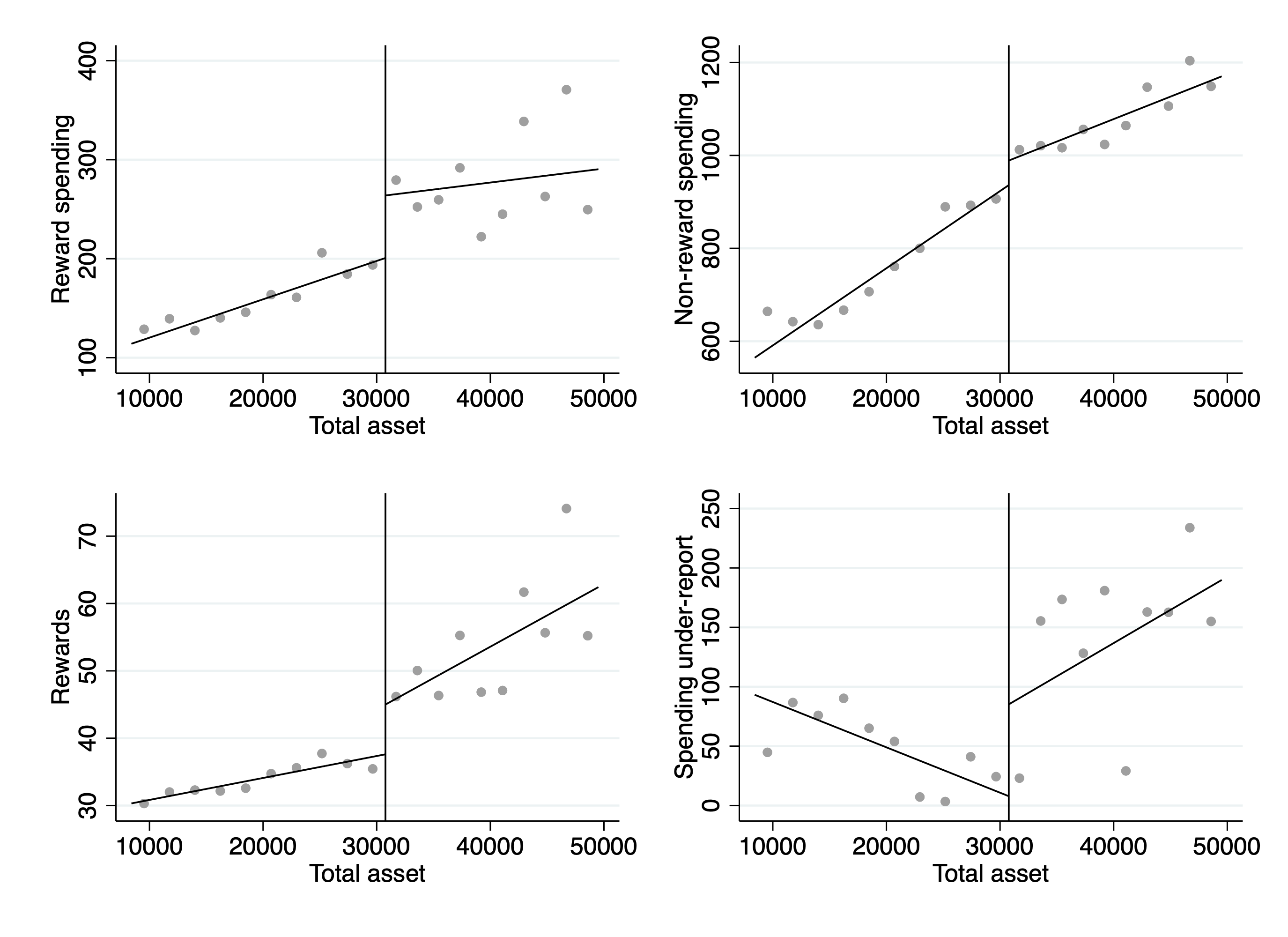

“Rewards and Misperceived Spending: Experimental Evidence from Credit Cards,” January 2026, Major Revision at Marketing Science (draft)

Abstract

Using proprietary data, a survey, and an experiment with a major bank in China, this paper studies how credit card rewards affect perceived and actual consumer spending. A larger reward variety increases spending in both rewarded and unrewarded categories. While consumers accurately predict rewarded spending, they tend to underestimate total spending. A potential channel is that consumers overlook follow-on purchases that are complementary to the initial rewarded purchases. This misperception distorts consumption and incentivizes firms to offer excessive rewards, generating cross-subsidies from naive to sophisticated consumers.

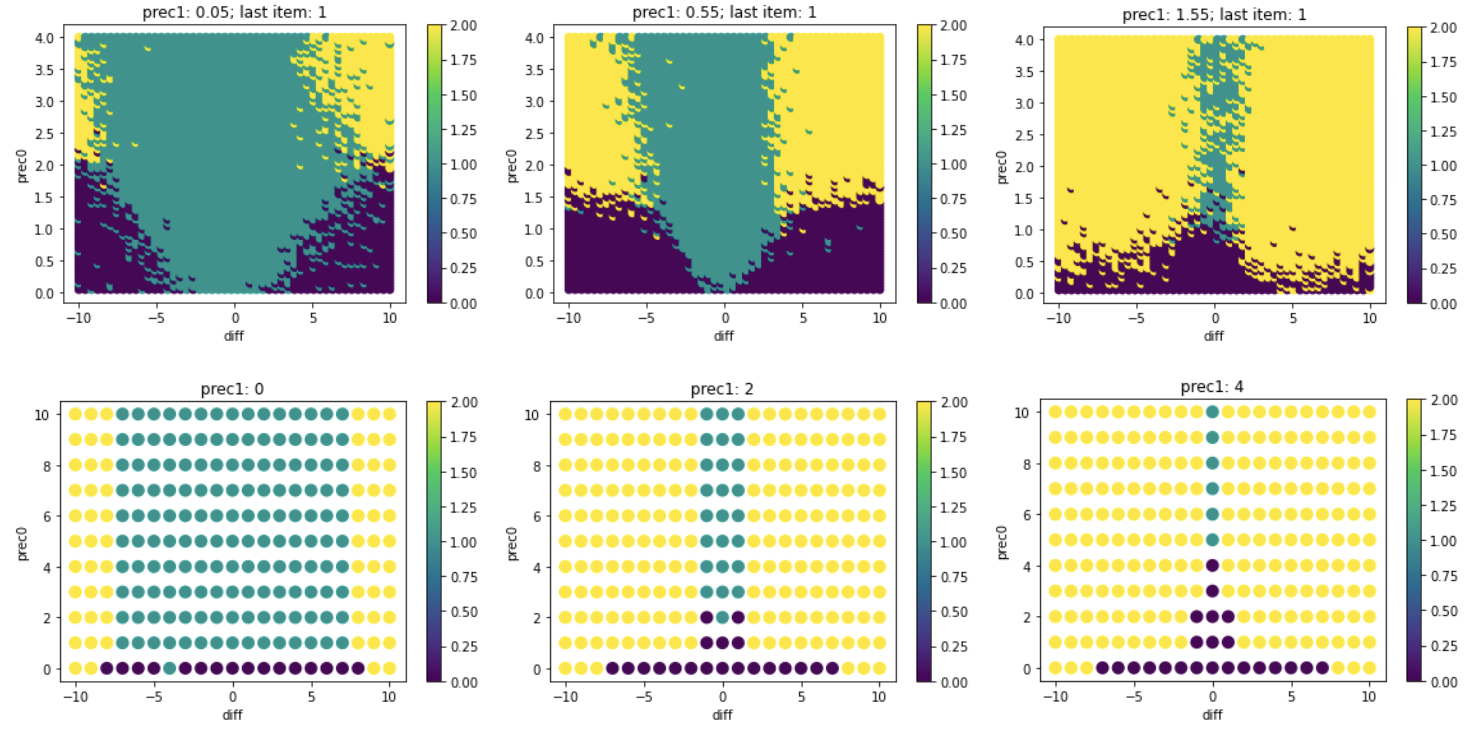

“An Empirical Model of Endogenous Attention,” with T. Tony Ke and J. Miguel Villas-Boas, September 2025 (draft)

Abstract

Before making a choice, individuals can gradually gather information on multiple different possible alternatives. Analysts may observe how long individuals spend gathering information on each alternative, when they switch from one alternative to another, and when they ultimately make their final choice. We develop an empirical model on this choice process, endogenizing the choice of which alternative the individual obtains information from at each point in time, and estimate the model with data from eye-tracking experiments. The empirical analysis yields estimates of the relative size of search costs, attention switching costs, and informativeness of search for information. Counterfactual analysis shows that higher attention switching costs reduce search duration and induce fewer attention switches; in comparison, higher search costs also reduce search duration but induce more attention switches. The model also delivers that there is a positive correlation between attention to an alternative and the likelihood of that alternative being chosen, through the individuals choosing to learn more about the alternatives for which the individuals have beliefs of a higher preference.

Work in Progress

“Income Misreporting in the Credit Card Market,” with Xiao Yin

Abstract

(Preliminary) In the process of acquiring credit cards, consumers often self-report their income levels, a practice that tends to be prone to unverified overstatements. We empirically investigate into the existence of such income misrepresentation and assess whether financial institutions take this potential exaggeration into account. Collaborating with a leading commercial bank in China, we survey consumers on their income growth rates. By utilizing these reported growth rates and current incomes, we infer the consumers' actual income at the time of their credit card application. Our findings indicate a significant degree of income over-reporting among consumers, with an average exaggeration of approximately 30%. Further, we employ a quasi-experimental approach to determine the causal effect of this income misreporting on the allocation of credit limits. Our results suggest that the bank does, in fact, take into account such misreporting behaviors: income exaggerated by 10% decreases credit limit by around 100 US dollars. This study provides insights into consumer behaviors in credit card applications and the corresponding response of financial institutions.

“Information Silos on Social Media,” with Wenbo Wang and Zijun (June) Shi

Abstract

(Preliminary) Social media platforms often confine users to information silos, creating narrow loops of reinforced interests that limit exposure to diverse perspectives and exacerbate societal divisions. This study introduces a metric to systematically quantify this phenomenon through two dimensions: intrapersonal variety, reflecting the breadth of individual topic engagement, and interpersonal difference, capturing the divergence of user consumption from population norms. Focusing on TikTok, we combine demographic surveys with a field experiment wherein participants record their browsing behavior. We analyze video topics to compute this information silo index, identify silo formation patterns, and correlate them with user characteristics. Furthermore, we test experimental interventions by providing users with tailored feedback on their content consumption habits. Our results demonstrate the intensity of information silos, assess user awareness, and establish the efficacy of feedback mechanisms in disrupting these patterns to foster broader content engagement.